The introduction of Corporate Tax in the UAE marked a significant shift in the country’s economic landscape. However, the UAE government remains committed to fostering a supportive environment for startups and SMEs. One of the most critical tools for this is Small Business Relief (SBR).

In this post, we break down what SBR in the UAE is, who can claim it, and the important deadlines you need to know.

1. What is Small Business Relief (SBR)?

Under Ministerial Decision No. 73 of 2023, Small Business Relief allows eligible UAE resident taxable persons (including certain natural persons with UAE business income) to be treated as having “no taxable income” during a tax period. Note that non-resident persons with only UAE-sourced income generally do not qualify in the same way.

The Key Benefits of Small Business Relief (SBR)

• 0% Corporate Tax:

You will not be required to pay the standard 9% corporate tax on your profits.

• Simplified Filing:

You must still file a CT return (SBR does not replace filing), but you may be allowed to file a Simplified Tax Return, subject to FTA rules at the time of filing.

• Accounting Flexibility:

Eligible businesses can use Cash Basis Accounting instead of the more complex Accrual Basis.

• Reduced Documentation:

You are not required to maintain exhaustive Transfer Pricing documentation, though reasonable support for related-party pricing and general arm’s-length principles must still be kept.

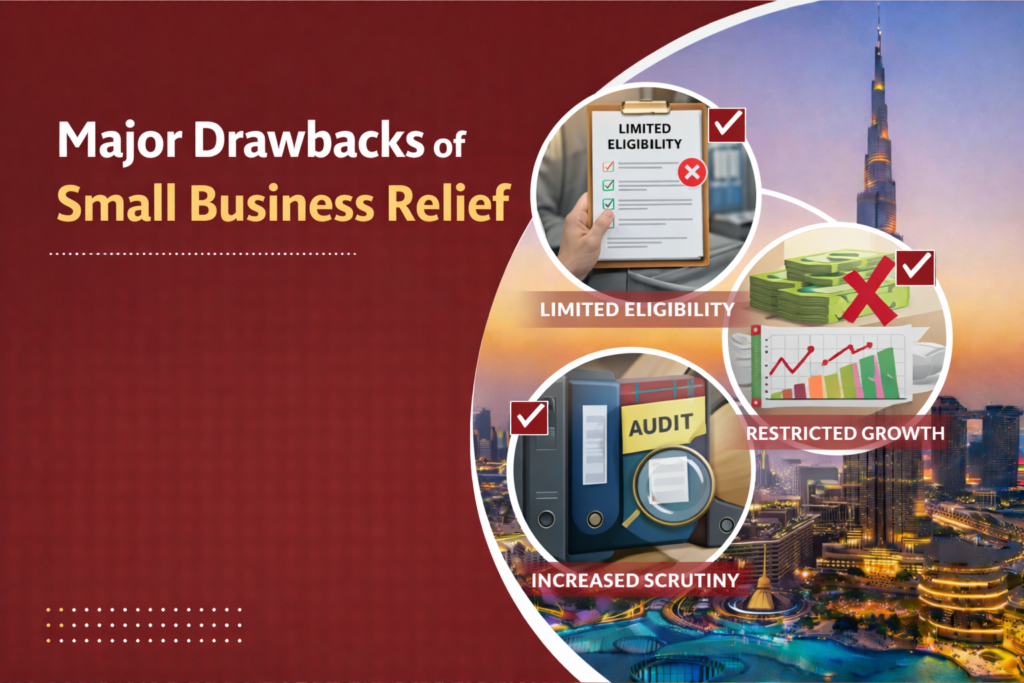

Major Drawbacks of Small Business Relief (SBR)

• No Loss Carryforward:

Cannot save tax losses to reduce future years’ taxable profits.

• No Interest Deductions:

Interest expenses become non-deductible, unlike normal CT rules, with the 30% EBITDA limit.

• Permanent Exit Risk:

Revenue over AED 3 million ends eligibility forever, even if it drops later—plus anti-abuse checks on business splitting.

• Still Need Records:

Keep invoices and bank statements for 7 years despite simplified rules.

2. Who is it Applicable to? (Eligibility Criteria)

To benefit from SBR, a business must meet the following four conditions:

► The Revenue Threshold

Your gross revenue (calculated according to applicable accounting standards, from all domestic and foreign sources—not profit) must be AED 3 million or less for the relevant tax period and all previous tax periods.

Note: Artificially splitting businesses to stay under AED 3 million can be challenged under anti-abuse rules. If your revenue exceeds AED 3 million in any tax period, you lose your eligibility for SBR for that period and all future periods, even if your revenue drops below the threshold later.

► The “Opt-In” Requirement

SBR is not automatic. You must actively elect to apply for the relief when filing your Corporate Tax return via the EmaraTax portal.

► Exclusions (Who cannot apply?)

You are ineligible for SBR if you are:

• A Qualifying Free Zone Person (QFZP) is already benefiting from the 0% preferential rate on qualifying income.

• A member of a Multinational Enterprise (MNE) Group with a consolidated global revenue exceeding AED 3.15 billion.

Freelancers and sole proprietors conducting business activities and crossing CT registration thresholds can also claim SBR, not just LLCs.

3. Applicability Timeline

The SBR is a temporary relief measure designed to help businesses transition into the tax regime.

• Start Date: It applies to tax periods starting on or after 1 June 2023.

• End Date: It is currently available for tax periods ending on or before 31 December 2026.

4. Important Trade-offs to Consider

| SBR Return | UAE CT Return |

You pay 0% tax regardless of profit. | You pay 0% on profits up to AED 375,000 and 9% thereafter. |

You cannot carry forward tax losses to future years. | You can carry forward losses to offset future taxable profits. |

| You cannot deduct interest expenses. | You can deduct interest (subject to the 30% EBITDA cap). |

| Simplified record-keeping. | Full compliance and audited financials may be required. |

Checklist for the return

1. Register: Even if you qualify for SBR, you must register for Corporate Tax and obtain a TRN.

2. Monitor Revenue: Keep a close eye on your “Gross Revenue” (not profit) to ensure it stays below AED 3 million.

3. Elect in Return: Ensure your accountant checks the SBR box during the annual filing.

4. Keep Records: Maintain your invoices and bank statements for at least 7 years.

Is your business approaching the AED 3 million threshold, or are you unsure if SBR is the right choice for your long-term tax strategy? At TAP Fiscal, we can conduct a professional eligibility assessment and handle your EmaraTax filings to ensure you stay compliant while maximizing your savings. Contact us today for a consultation.

Ready to start your venture? Contact TAP Fiscal today.

Frequently Asked Questions (FAQs)

Commonly searched questions on UAE Small Business Relief (SBR) cover eligibility, revenue rules, filing, and comparisons, based on top FAQs and guides.

(Eligibility Criteria)

What is Small Business Relief (SBR) in UAE Corporate Tax?

SBR treats eligible UAE resident businesses as having no taxable income for a tax period, resulting in 0% corporate tax and simplified compliance.

Who qualifies for SBR?

UAE resident persons (juridical or natural) with revenue ≤ AED 3 million in the current and all prior tax periods, not part of an MNE group (global revenue ≥ AED 3.15 billion), and not a Qualifying Free Zone Person.

Does SBR apply to freelancers or sole proprietors?

Yes, resident natural persons conducting business in the UAE qualify if revenue is ≤ AED 3 million and other conditions are met.

Can Free Zone businesses claim SBR?

Non-QFZP free zone residents can if under revenue limit; QFZPs are excluded as they get 0% on qualifying income.

(Revenue Threshold)

What counts as revenue for the AED 3 million SBR threshold?

Total gross revenue per accounting standards (IFRS/Cash Basis), including sales, services, and commissions from all sources before costs, non-taxable items like UAE dividends still count.

What if revenue exceeds AED 3 million once—can SBR resume later?

No, eligibility ends permanently for that period and all future ones, even if revenue drops.

Can multiple related businesses claim SBR separately?

Each entity qualifies independently unless in a tax group, which shares the AED 3 million limit.

(Application and Filing)

How do you apply or elect SBR?

No separate form opt-in by checking the box on your Emara Tax CT return for each period.

Must you register for CT and file under SBR?

Yes, obtain a TRN and file a return even with 0% tax; simplified but not exempt from filing.

What documents are needed for SBR filing?

Financial statements, revenue proof (invoices/bank statements), eligibility declaration, expense records; retain 7 years.

(Timeline and Trade-offs)

When does SBR end?

Available for tax periods ending on or before 31 December 2026; “use it or lose it” opportunity.

SBR vs 0% CT threshold—which is better?

SBR for ≤ AED 3M revenue (0% tax, simpler, no losses/interest); 0% threshold for profits ≤ AED 375K with full deductions.

What are the SBR drawbacks?

No loss carryforward, no interest deductions, permanent loss if threshold breached; simpler records but still 7-year retention.