In the ever-evolving real estate landscape of the UAE, understanding the tax implications of property is no longer just for accountants; it’s essential for every investor, landlord, and business owner. Whether you are renting out a single office or buying a multi-million dirham warehouse, the rules for 2026 are clear.

At TAP Fiscal, we specialize in making these complex tax journeys simple. Here is our guide to navigating VAT in the UAE property market.

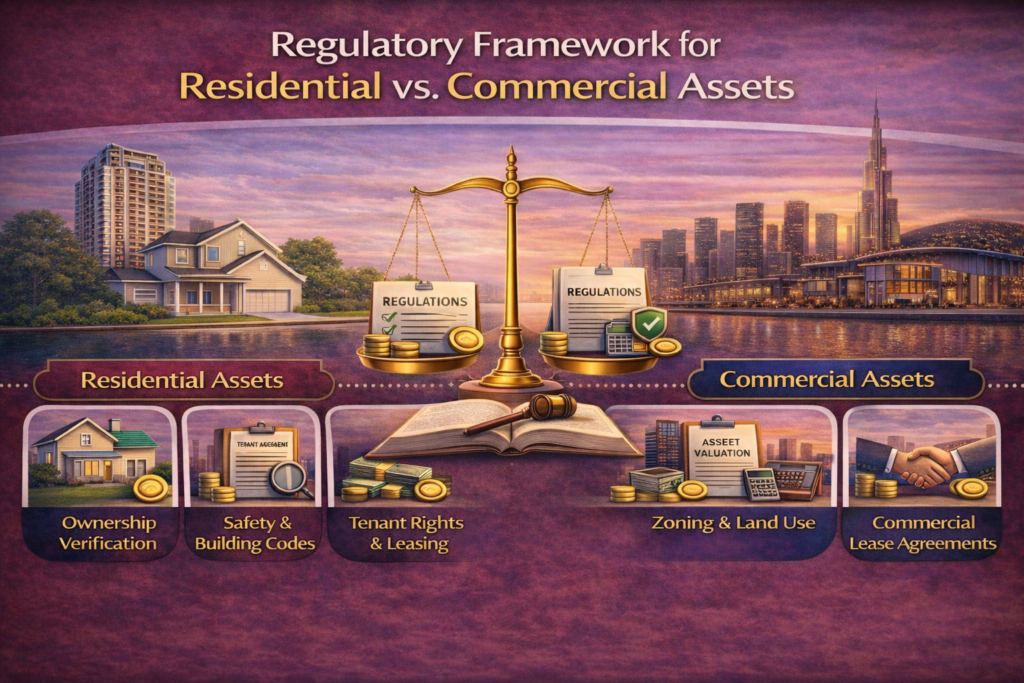

1. The Regulatory Framework: Residential vs. Commercial Assets

The first thing you need to know is that the UAE treats “home” and “work” very differently when it comes to tax.

Residential Property:

Residential property is generally exempt from VAT. Whether you are buying a villa or renting an apartment for personal use, the transaction is typically VAT-exempt, meaning no 5% VAT is added to the purchase price or rent.

Note: The first supply of a newly constructed residential property by a developer is zero-rated (0%), but subsequent sales or leases are usually VAT-exempt.

Commercial Property:

This includes offices, retail shops, warehouses, and even bare land. Unlike your home, these are Standard-rated at 5%. Whether you are selling or leasing, the 5% VAT must be part of the conversation.

2. How to Save on VAT (Even if your property is under AED 5 Million)

The most effective way to acquire commercial property without paying the 5% VAT upfront is by utilizing the Transfer of a Going Concern (TOGC) provision. When an investor asks, “Can I avoid VAT if the property is already rented?” the answer is a definitive yes.

Under the UAE VAT Law, a TOGC is classified as being “outside the scope of VAT.” Because the law views this as the transfer of an active business rather than a simple sale of a “supply,” the 5% VAT is not triggered. This means the seller collects no tax, and no payment is required from the buyer.

Conditions to Qualify for TOGS: To secure this tax-free status, four specific criteria must be satisfied:

Operational Business Transfer:

You must be acquiring an active rental business (a tenanted unit), not a vacant “shell” or empty property.

Mandatory vs. Voluntary Registration:

Mandatory registration (taxable income > AED 375,000): You must have submitted your VAT registration application to the FTA before the property transfer date.

Voluntary registration (taxable income > AED 187,500): You must be fully registered with an active TRN before the transfer. A pending voluntary application does not always guarantee TOGC protection.

Continuity of Activity:

The purchaser must intend to continue the same economic activity—specifically, leasing the property—after the transfer.

Legal Documentation:

Both parties must formally declare their intent to treat the transaction as a TOGC within the Sale and Purchase Agreement (SPA).

3. Voluntary Registration (No Trade License Needed!)

A major misconception among private investors is that you need a company or a trade license to interact with the Federal Tax Authority (FTA). This is not the case. Even if you only own a single small shop and your rental income is modest, you can and often should voluntarily register for VAT.

Registration Without a Trade License or Title Deed

The FTA recognizes that leasing commercial property is a valid “economic activity” in its own right. You can voluntarily apply for registration if your taxable turnover (rental income) or your taxable expenses (legal fees, commissions, or the property purchase itself) exceed AED 187,500.

- No Title Deed Required: You do not have to wait for the final deed to start the process. You can apply for VAT registration using a signed Sale and Purchase Agreement (SPA) or MOU as evidence that you are in the process of acquiring a taxable asset.

- No Trade License Required: You do not need to set up a formal company. You can be registered as a “Natural Person” using your personal identity documents.

Registering as a “Natural Person”

At Tap Fiscal, we specialize in helping individual landlords secure their Tax Registration Number (TRN) under the “Natural Person” category. This allows you to:

- Recover the 5% VAT paid on the purchase of the property.

- Offset VAT on maintenance, service charges, and refurbishment costs.

- Ensure Compliance for a Transfer of a Going Concern (TOGC) before the title transfer happens.

Documents we use for your application: Your Emirates ID, Passport, and the SPA/MOU for your upcoming property purchase.

4. High-Value Assets: The Capital Asset Scheme (CAS)

For properties valued at AED 5 million or more, the UAE applies the Capital Asset Scheme. This is a long-term regulatory framework designed to ensure that VAT recovery accurately reflects the property’s use over its lifetime.

Criteria for the Capital Asset Scheme

To be classified under this scheme, a property must meet the following strict criteria:

- Value Threshold: A single item of expenditure (or staged payments for one project) totaling AED 5 million or more, exclusive of VAT.

- Asset Type: Specifically for buildings or parts of buildings (including extensions and major refurbishments).

- Estimated Useful Life: The asset must have an intended business life of at least 10 years.

- Staged Payments Rule: If you spend smaller amounts on a single construction project or a major renovation that eventually crosses the AED 5 million mark, the entire project is treated as a single capital asset.

How the Scheme works

1. Immediate 100% Recovery

If you are VAT-registered and your intended use for the building is entirely taxable (e.g., leasing it out as a commercial office), you are eligible to recover the full 5% VAT in your first tax return.

Example: On an AED 10 million property, you pay AED 500,000 in VAT. Under this scheme, you can claim that entire amount back from the FTA immediately to protect your cash flow.

2. The 10-Year Adjustment Period

Each year, you must review whether the property’s usage still qualifies for the VAT you recovered.

If the building remains 100% commercial for all 10 years, you keep the full refund.

If the usage changes, an annual “adjustment” is made in your VAT return to repay or recover a portion of the tax.

3. Change of Use & Repayment

If you alter the property’s purpose for example, converting a commercial floor into a private residence (which is exempt) you must perform an adjustment.

The Example: If in Year 6 you change the use to “exempt,” you must calculate the “lost” taxable usage and pay back a pro-rata portion of that initial AED 500,000 refund to the FTA for each remaining year in the 10-year cycle.

4. Record-Keeping for 2026

Because this scheme spans a decade, the standard 5-year record-keeping rule does not apply. For any property under the Capital Asset Scheme, you are legally required to maintain all invoices, contractsand usage records for 15 years.

5. Critical Rules for 2026

The “Special Payment” Rule (SPM)

When buying a commercial property from anyone other than the developer, the seller doesn’t collect the tax. Instead:

- The Buyer pays the 5% VAT directly to the FTA portal.

- You get a Payment Transaction Number (PTN).

- The Land Department will not transfer the title to your name without this PTN.

6. Stricter Limits

Starting in 2026, the FTA will be stricter. You now have a 5-year limit to claim any refunds you are owed. Additionally, for Capital Assets (over 5M), you must keep your records for 15 years.

How Tap Fiscal Can Help

Navigating the FTA portaland determining eligibility for TOGC or the Capital Asset Schemecan be complex and time-consuming. At Tap Fiscal, we take care of the technical details so you can focus on your investment with confidence.

From obtaining your Property Transfer Number (PTN) to managing the required 15-year record-keeping, we act as your trusted partner for UAE VAT compliance every step of the way.

Looking to secure your VAT refund or need a PTN for your next property purchase? Schedule a one-on-one consultation today!

📞Phone: +971 502890630

📧Email: info@tapfiscal.com

🌐Website: www.tapfiscal.com

Frequently Asked Questions (FAQs)

Q1: Is there any VAT on residential rent?

A: No. Residential rent is exempt from VAT. Landlords don’t charge it, and tenants don’t pay it.

Q2: What exactly counts as “Commercial Property”?

A: Any building or land that isn’t residential, including offices, retail shops, warehouses, hotels, and bare land.

Q3: Can I avoid paying the 5% VAT if the property is already rented?

A: Yes! Through a Transfer of a Going Concern (TOGC). If you are VAT-registered and buying a tenanted building to continue the leasing business, the sale is “outside the scope of VAT.”

Q4: I only own one small office. Do I really need to register for VAT?

A: If your rent is above AED 375,000, it’s mandatory. Above AED 187,500, it’s voluntary. Voluntary registration is popular because it allows you to recover the VAT you paid on the purchase and maintenance.

Q5: How do I pay VAT when buying from a private seller?

A: Use the Special Payment Mechanism (SPM). You pay the FTA directly through the EmaraTax portal to get your PTN, which is required for the title transfer.

Q6: I paid 5% VAT on a 6-million-dirham warehouse. Can I get that money back?

A: Yes. As it is a Capital Asset (>5M), you can claim the full amount back if you are VAT-registered and using it for business.

Q7: What happens if I use my building for both business and living?

A: This is a “Mixed-Use” property. You charge 5% VAT on the office part and 0% on the apartment part. Expenses like roof repairs must be apportioned (e.g., if it’s 50/50, you only claim 50% of the VAT back).

Q8: How long do I need to keep my records?

A: For most, 5 years. For real estate, you must keep records for 15 years.

Q9: What if I forget to register for VAT on time?

A: Late registration carries an automatic AED 10,000 penalty, plus fines for every missed tax return.

Q10: Can I claim back VAT on a property I bought 3 years ago?

A: Yes, as long as it’s within the 5-year limit for refunds. Don’t wait until 2026 passes!

Q11: How do I get a Payment Transaction Number (PTN)?

A: A PTN is obtained through the FTA’s EmaraTax portal under the Special Payment Mechanism and must be submitted correctly to avoid delays—Tap Fiscal manages the entire process for you to ensure full compliance.

Q12: What happens if I sell my Capital Asset early (before 10 years)?

A: If you sell it as a taxable supply (charging 5% VAT), you generally keep your refund. If you convert it to residential or use it personally, you must pay back a pro-rata portion of the refund.

Q13: Do I need a trade license to register for VAT?

A: No. You can register as a “Natural Person.”